Inside Africa’s $330 Billion SME Financing Gap: 15 African SME Fintech Startups Changing Access to Capital

Africa’s $330 billion SME financing gap is fueling a powerful wave of fintech innovation. This article breaks down 15 African SME fintech startups changing how merchants, freelancers, and informal traders access capital.

Inside Africa’s $330 billion SME financing gap, a new wave of african sme fintech startups is making it easier for small businesses to get capital, manage cash flow, and keep growing. Recently selected by Renew Capital, these startups are building practical tools for merchants, freelancers, and informal traders who often struggle to access traditional bank loans.[1][6]

Moreover, the story is bigger than funding alone. Across Africa, fintech now drives a large share of startup investment, and the strongest players are not just moving money; they are solving the daily problems of payments, inventory, lending, and record-keeping.[2][4][9]

Why Africa’s SME financing gap matters

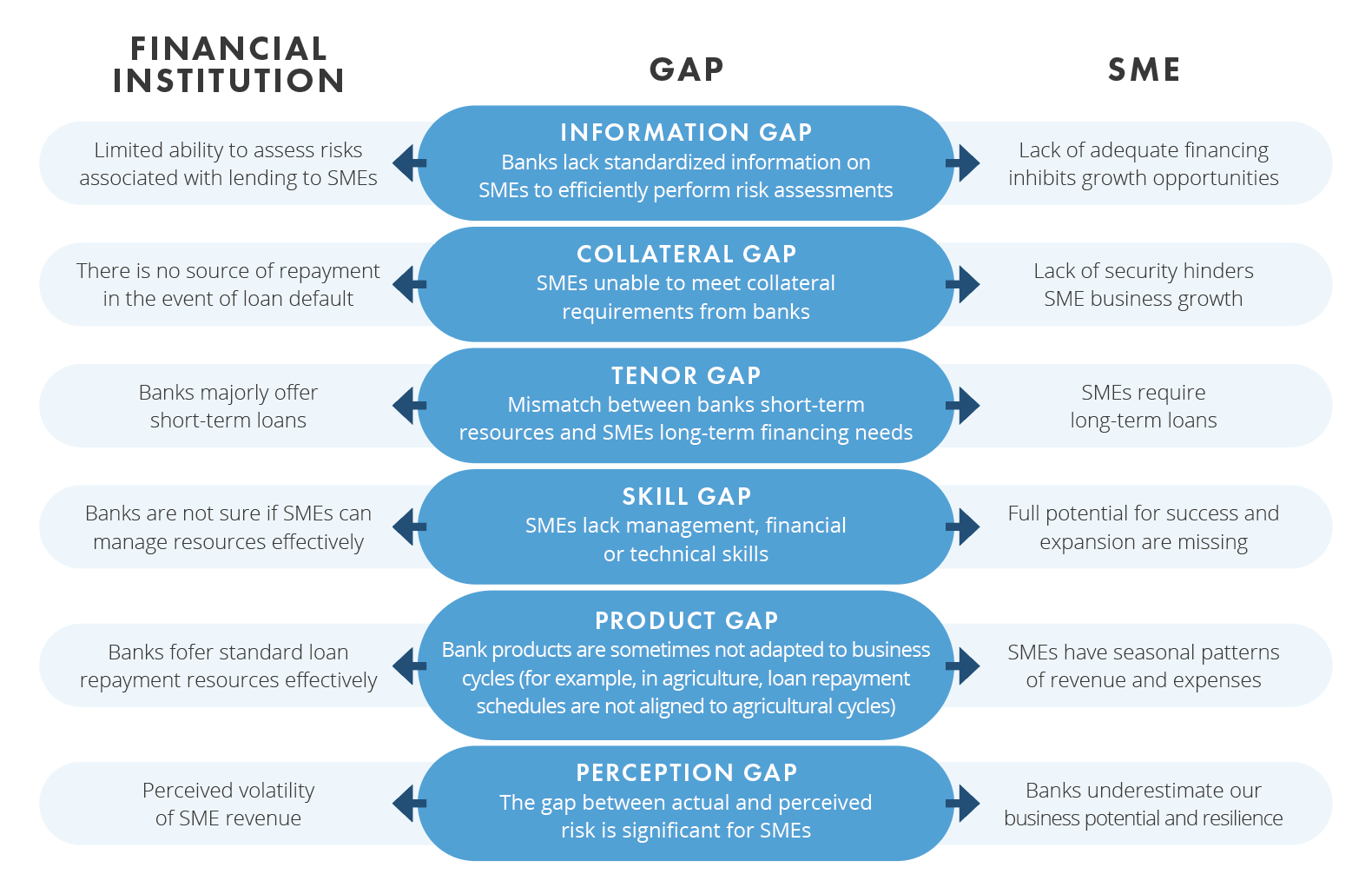

Africa’s small and medium-sized businesses sit at the center of jobs, trade, and local supply chains. However, many still operate outside formal banking systems, which makes it harder to prove income, build credit history, or qualify for loans.[6][7]

Consequently, many owners rely on savings, family support, rotating savings groups, or expensive informal lenders. That gap slows expansion, limits stock purchases, and weakens resilience when sales fall or seasons change.[6][7]

Additionally, the financing problem is not only about loan size. Small businesses often need faster payment tools, better record keeping, and access to working capital that fits real business cycles, not rigid bank terms.[4][7]

- Working capital helps businesses buy stock and cover short-term costs.

- Digital records help lenders assess risk more fairly.

- Alternative finance gives access to capital without long bank delays.

For readers following African business trends, this is also a major innovation story. Explore more on Business & Economy, Technology, and Africa News for more coverage of the continent’s growth sectors.

How African SME fintech startups are changing the game

In particular, the best african sme fintech startups are building around how African commerce already works. They support mobile money, informal retail, cross-border trade, and micro-merchant activity rather than forcing businesses into foreign-style banking models.[4][6][10]

Furthermore, these companies are using data from transactions, cash flow, sales patterns, and digital records to evaluate creditworthiness. That means a tailor, salon owner, delivery rider, or kiosk trader may qualify for financing even without a traditional bank statement.[3][7][10]

Meanwhile, Renew Capital’s selection signals growing investor interest in practical, revenue-linked fintech models. The group reflects a wider shift in African startup funding toward tools that help SMEs survive and scale in real market conditions.[1][12]

What these startups typically do

Most of the selected startups fall into a few clear models. Some lend directly, some help merchants collect payments, and others build the infrastructure lenders need to make smarter decisions.[3][4][7]

- Digital lending for quick business cash.

- Payments and collections for merchants and informal traders.

- Credit scoring and risk tools for lenders and MFIs.

- Business management tools that improve records and cash flow visibility.

15 African SME fintech startups to watch

Below are 15 names often discussed in Africa’s fintech and SME finance space, including companies highlighted in recent coverage of the sector and the Renew Capital-backed momentum around small business finance.[1][3][4][7][9]

1. Moniepoint — Nigeria

Moniepoint has become one of the clearest examples of SME-first fintech in Africa. It serves merchants with payment tools, business banking services, and lending support built around daily business operations.[2][4]

Importantly, it shows how payments data can become a route to credit. For many Nigerian businesses, that combination makes capital easier to access and easier to repay.[2][4]

2. Pezesha — Kenya

Pezesha focuses on solving the working-capital challenge for small businesses. It uses digital infrastructure and partner networks to connect SMEs to financing options that match their cash flow.[3][6]

Additionally, its model reflects a broader trend in Africa: lending based on real transaction data, not just collateral.[3][7]

3. Numida — Uganda

Numida helps small businesses digitize records and use those records to unlock unsecured loans. That matters because many informal businesses have income, but little paperwork.[7]

Therefore, the startup turns everyday business activity into a financial profile lenders can understand.[7]

4. Lulalend — South Africa

Lulalend offers digital lending for SMEs that need faster access to business capital. It has built a strong reputation for tech-driven underwriting and quick funding decisions.[3]

Moreover, it represents the kind of modern credit platform that suits businesses with urgent inventory or payroll needs.[3]

5. Zoona — Zambia

Zoona supports payments, transfers, and agent-based financial services across underserved markets. Its network approach gives entrepreneurs a way to earn income while extending financial access in their communities.[3][8]

In particular, the agent model is powerful in places where branches are scarce and trust matters.[3][8]

6. ClickPesa — Tanzania

ClickPesa provides digital business tools and payment services that help SMEs collect money more efficiently. It is especially useful for merchants who need reliable payment rails for everyday transactions.[3]

Consequently, it helps reduce the friction that often slows trade in cash-heavy markets.[3]

7. Awamo 360 — Kenya

Awamo 360 is designed for microfinance institutions and their clients. It offers a digital platform that helps lenders manage operations and better serve small borrowers.[3]

Furthermore, that kind of infrastructure can improve how microloans are tracked, approved, and repaid.[3]

8. Fawry Microfinance — Egypt

Fawry Microfinance focuses on merchants and SMEs that need tailored financial products. Its model shows how large payment ecosystems can expand into small business finance.[4]

Meanwhile, Egypt remains one of Africa’s most important fintech markets because merchants need scalable payment and lending tools.[4]

9. Kopo Kopo — Kenya

Kopo Kopo helps SMEs accept and analyze mobile payments. It also supports customer engagement, which matters when small businesses need repeat sales and stronger margins.[10]

Additionally, its platform shows how payments data can become a business growth tool, not just a checkout tool.[10]

10. M-Changa — Kenya

M-Changa is best known for crowdfunding and collective fundraising. For small businesses, that can mean community-backed capital for stock, equipment, or short-term needs.[10]

As a result, it offers an alternative to formal credit, especially for businesses with strong local networks.[10]

11. Cellulant — Kenya and Nigeria

Cellulant operates a major payments ecosystem across multiple African markets. It connects merchants, banks, and mobile operators, making it a core enabler of commerce.[10]

Moreover, platforms like this often sit behind the scenes, powering the payment flows SMEs depend on every day.[10]

12. Klasha — Nigeria

Klasha focuses on cross-border payments and emerging-market commerce. That makes it useful for traders and online sellers working across African markets and beyond.[1]

Importantly, the cross-border angle matters for SMEs that import stock or sell to customers in other countries.[1]

13. eShandi — Zambia

eShandi started as PremierCredit and has evolved into a broader fintech platform. It aims to improve how people access and manage money, with strong relevance for small business users.[1]

Furthermore, its evolution reflects a common African fintech path: start with lending, then expand into wider financial services.[1]

14. CASHPLUS — Morocco

CASHPLUS offers money transfers, currency exchange, and financial services that support everyday commerce. For SMEs, that kind of infrastructure can reduce payment delays and improve liquidity.[3]

Additionally, North African fintech continues to show how digital finance can support both retail users and small firms.[3]

15. Nomanini — South Africa

Nomanini serves informal merchants with payment tools built for cash-based retail. That makes it especially relevant in markets where small shops still handle a large share of daily transactions.[10]

Therefore, it speaks directly to the realities of township retail, informal trade, and low-margin selling.[10]

What these platforms mean for merchants, freelancers, and informal traders

For merchants, the biggest win is speed. They can collect payments faster, restock sooner, and avoid missing sales because of cash shortages.[4][7]

However, the impact goes beyond shop owners. Freelancers and gig workers can use some of these tools to smooth income, save consistently, and qualify for small loans when client payments arrive late.[7][10]

Meanwhile, informal traders often benefit most from simple features like payment links, mobile collections, and digital records. Those features create a financial trail that can later support a larger loan or better terms.[7][10]

- Merchants gain faster sales and working capital.

- Freelancers gain income tools and short-term cash support.

- Informal traders gain records, payments, and loan visibility.

Why investors are paying attention now

Notably, African fintech remains one of the continent’s strongest startup sectors for investment and growth. Recent coverage shows continued investor interest in payments, lending, regtech, and cross-border commerce tools.[2][9][12]

Moreover, global and regional investors increasingly back startups that solve clear market pain points. In Africa, that means products that work with mobile money, informal commerce, and fragmented financial systems.[4][6][10]

Consequently, startups that help SMEs operate better tend to have a direct path to revenue. They serve businesses that need the service now, not a future use case.[1][4][9]

How African SME fintech startups can scale further

However, the next growth phase will require more than clever apps. These companies need strong compliance, partner networks, better risk models, and support across multiple countries.[6][12]

Additionally, many small businesses still need financial literacy, digital onboarding, and simple user interfaces. A strong product must work for first-time smartphone users as well as seasoned traders.[7][10]

Therefore, the winners will likely be the platforms that combine easy use, local trust, and clear business value. That is especially true in markets where cash still dominates and margins remain thin.[4][10]

What to watch next

Expect more movement in embedded finance, alternative credit scoring, merchant payments, and cross-border tools. Also expect more partnerships between fintech startups, MFIs, telcos, and local retailers.[1][4][12]

In addition, watch for more startup stories that blend business finance with creator-led commerce, social selling, and digital trade. Those spaces are becoming important for Africa’s young entrepreneurs and online sellers.

Discover more coverage of startups and small business growth in Technology, Business & Economy, and Culture & Lifestyle. Read more about the people building Africa’s future, and share your thoughts on which startup models will scale fastest.

Explore More on Topping Africa

For more stories on Africa’s fast-changing economy, explore these sections:

- Technology — startup trends, fintech, and digital tools shaping African business.

- Business & Economy — funding, trade, entrepreneurship, and market shifts across the continent.

- Africa News — the latest developments influencing growth, jobs, and innovation.

Suggested external reading: International Finance Corporation for SME finance context, GSMA Mobile for Development for mobile money trends, and Africa.com for broader continental business coverage.

Subscribe for more African innovation stories, and leave a comment below on which of these african sme fintech startups you think will reshape small business finance next.

Staff

Contributing writer at Topping Africa.

0 Comments

No comments yet. Be the first to share your thoughts!